Brushing Debt Off Your Shoulders

Brushing Debt Off Your Shoulders: A Hip-Hop Guide to Taking Control of Personal Debt

Understanding your rights, rebuilding your credit, and taking back financial control.

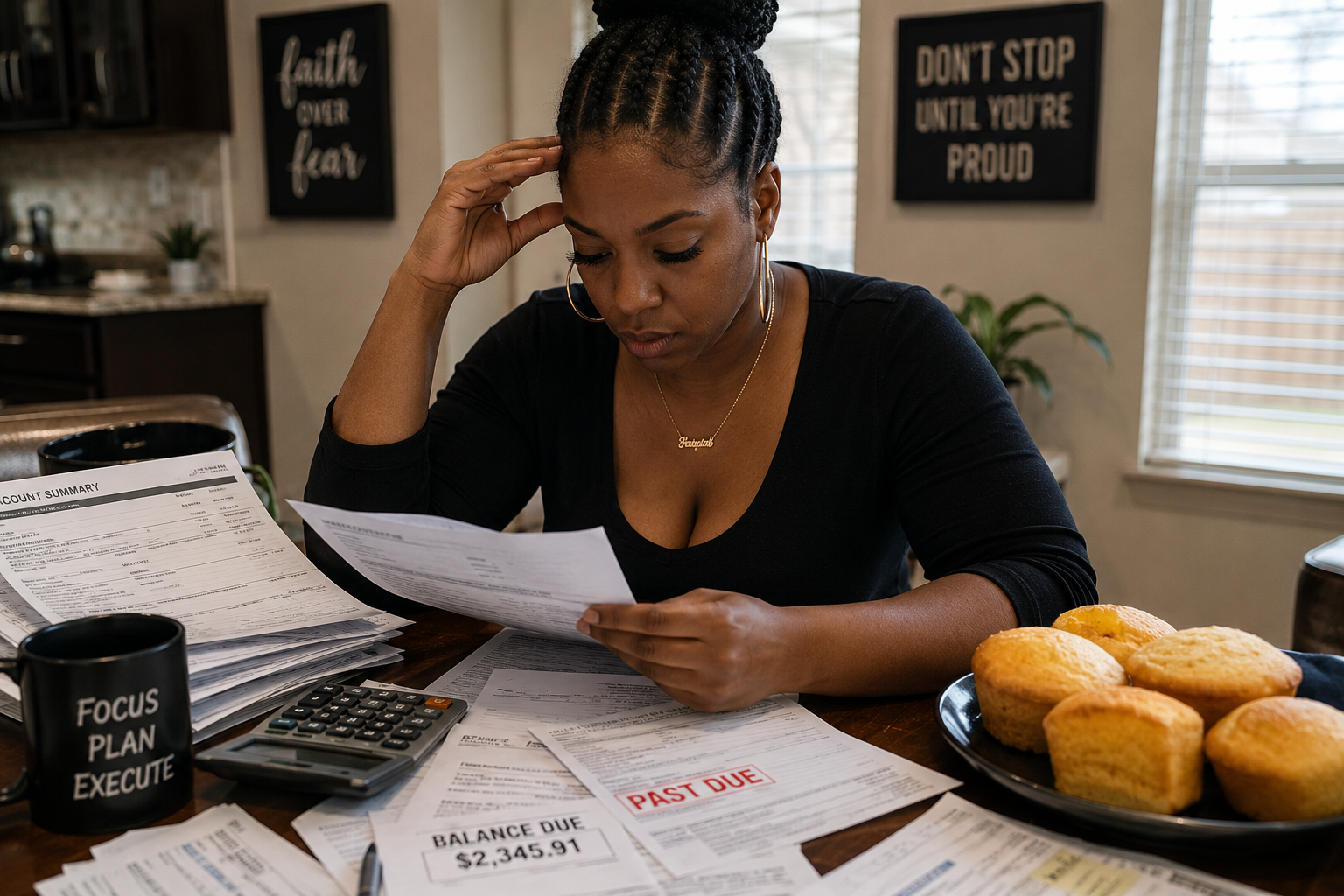

Debt can feel like a heavy beat looping in the background of your life — always there, always loud, always demanding attention.

For many people in the hip-hop community, financial struggles aren’t just statistics — they’re lived experiences. From paycheck-to-paycheck living to unexpected setbacks, debt can creep into your life and stay longer than an unwanted guest.

“Debt doesn’t have to define your future.”

Just like hip-hop was built on resilience, reinvention, and turning struggle into strength, managing personal debt is about reclaiming control.

Understanding the Weight of Personal Debt

Debt affects more than your bank account. It impacts your stress levels, relationships, confidence, and opportunities.

A damaged credit score can make it harder to:

- Rent an apartment

- Buy a vehicle

- Secure a business loan

- Qualify for better financial opportunities

Hip-hop culture has always reflected the realities of financial struggle. Lyrics about hustling, overcoming adversity, and building wealth from nothing resonate because they’re rooted in real life.

Why Debt Collectors Have So Much Power

Debt collectors purchase delinquent accounts for pennies on the dollar and attempt to recover as much money as possible.

Unfortunately, many consumers don’t know their rights. Some collectors rely on intimidation, repeated calls, misleading statements, or pressure tactics to collect debts quickly.

“Knowledge is leverage.”

What Is the FDCPA?

The Fair Debt Collection Practices Act (FDCPA) is a federal law created to protect consumers from abusive, deceptive, and unfair debt collection practices.

The FDCPA gives consumers powerful rights that can level the playing field.

Key Consumer Protections

- Collectors cannot harass you

- Collectors cannot lie or misrepresent debts

- You can request debt validation

- You can request communication in writing

- You can stop certain communication attempts

Recognizing Illegal Debt Collection Tactics

Some debt collectors cross legal boundaries hoping consumers won’t challenge them.

Watch for these red flags:

- Threats of jail time

- Pressure to pay immediately

- Refusal to provide written verification

- Calling family members excessively

- Threatening lawsuits they cannot legally file

If a collector violates the FDCPA, you may have grounds to sue for damages.

How to Respond When a Debt Collector Contacts You

The first conversation with a collector matters.

Don’t panic. Don’t admit ownership immediately. Don’t provide banking information too quickly.

Instead, slow the process down and gather information.

Validating the Debt

Ask for:

- Original creditor information

- Itemized balance details

- Proof the collector owns or can legally collect the debt

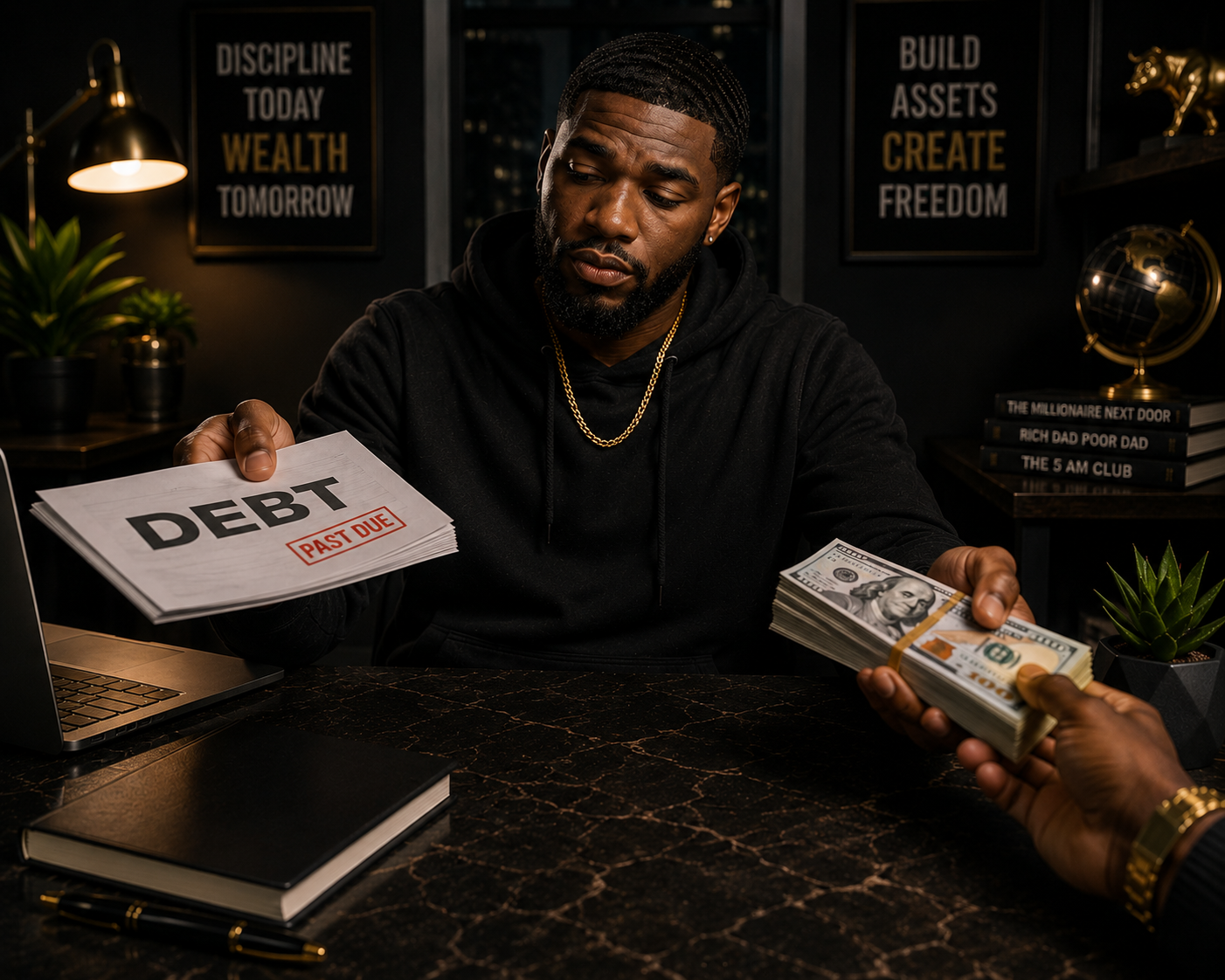

Negotiating Debt Settlements Like a Pro

Debt collectors often buy accounts cheaply, meaning they may accept less than the full balance.

Settlement negotiations are common.

Lump-Sum Settlements

Collectors may accept:

- 30%

- 40%

- 50%

of the original balance depending on account age and circumstances.

“Always get agreements in writing.”

Cleaning Collection Accounts From Your Credit Report

Negative collection accounts can remain for up to seven years, but inaccurate information can often be challenged.

Disputing Inaccurate Information

Under the Fair Credit Reporting Act (FCRA), consumers can dispute:

- Incorrect balances

- Duplicate accounts

- Accounts not belonging to them

- Incorrect payment statuses

Credit bureaus must investigate disputes.

Understanding Statutes of Limitations

Every state has a legal time limit for suing over debt.

Once expired:

- Collectors may still attempt collection

- But they generally cannot successfully sue

Before agreeing to anything, understand:

- Your state laws

- Account age

- Legal risks

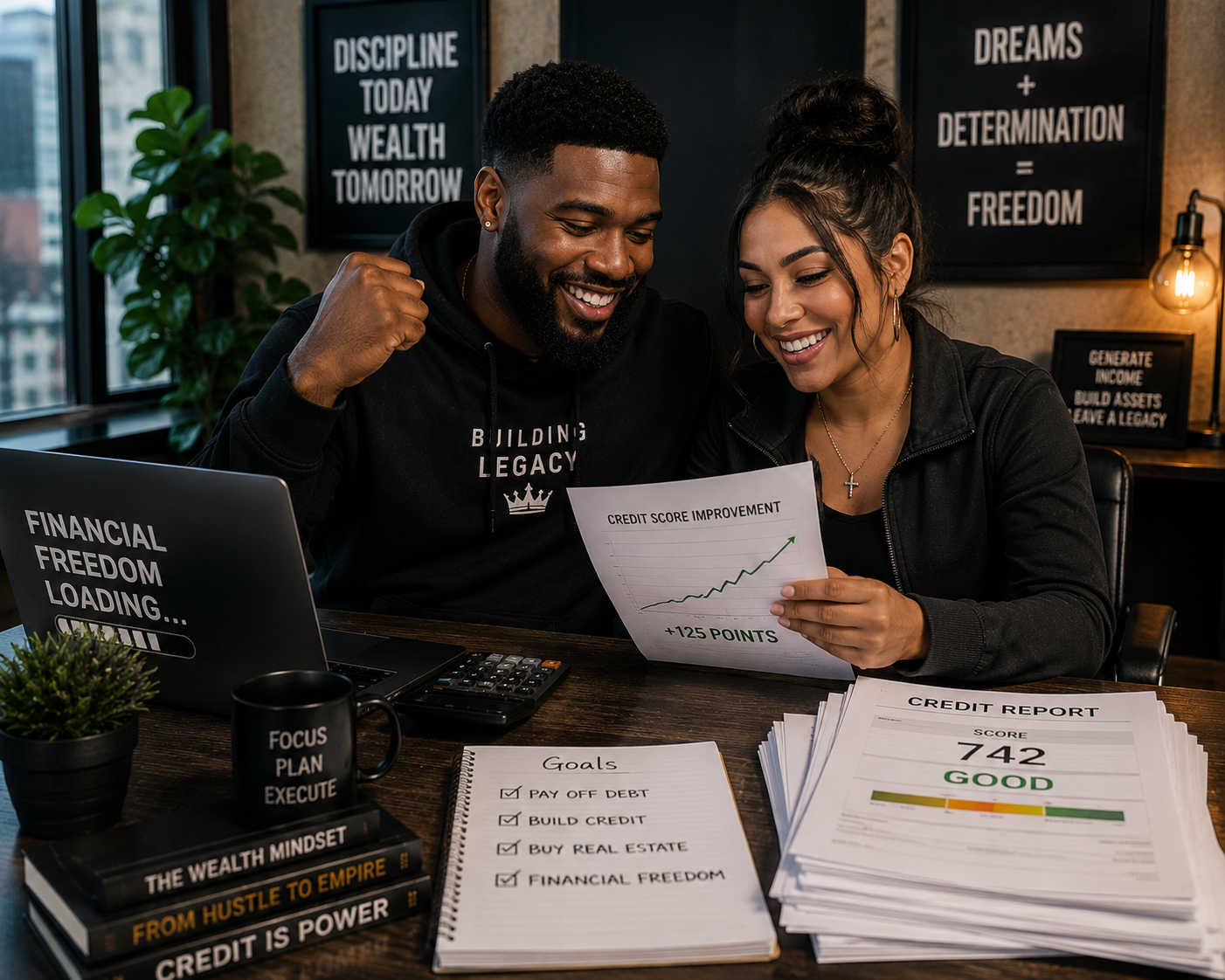

Building Financial Discipline After Debt

Getting out of debt is one chapter. Staying out of debt is another.

Financial discipline involves:

- Budgeting realistically

- Building emergency savings

- Limiting unnecessary spending

- Using credit strategically

Common Mistakes Consumers Make

- Ignoring debt collectors

- Paying without documentation

- Giving direct bank access

- Restarting old debt accidentally

- Falling for scare tactics

“Financial recovery takes patience, discipline, and knowledge.”

Conclusion

Brushing debt off your shoulders isn’t just about improving a credit score — it’s about reclaiming peace of mind, confidence, and financial freedom.

Understanding the FDCPA, negotiating strategically, validating debts, and cleaning inaccurate collection accounts from your credit report can change your financial future.

Hip-hop has always been about transformation — taking struggle and turning it into power. Financial recovery follows the same principle.

The process takes patience, discipline, and knowledge, but the weight of debt doesn’t have to stay on your shoulders forever.